OCI N.V. recommends the unsolicited all-cash Offer from NNS at EUR 4.10 per share. The Court-appointed Directors consent to the convocation of an extraordinary general meeting to submit the OCI-Orascom transaction to a shareholder vote.

|

AMSTERDAM, July 1, 2026 /PRNewswire/ -- OCI Global N.V. ("OCI" or the "Company") (Euronext: OCI) announces that the Board of Directors (the "Board") (excluding Nassef Sawiris and Nadia Sawiris) recommends the voluntary all-cash public offer (the "Offer") for all issued and outstanding shares in the share capital of OCI (each a "Share") at an offer price of EUR 4.10 cum dividend per Share made by NNS Holding (Cyprus) Limited ("NNS").

OCI N.V. recommends the unsolicited all-cash Offer from NNS at EUR 4.10 per share. The Court-appointed Directors consent to the convocation of an extraordinary general meeting to submit the OCI-Orascom transaction to a shareholder vote.

The court-appointed independent non-executive directors (the "Court-appointed Directors") of OCI announce that, having completed their assessment of the transaction between OCI and Orascom in conjunction with the NNS Offer, they have decided to consent to the convocation of an extraordinary general meeting of the Company to approve the OCI-Orascom transaction. The resolution to approve the OCI-Orascom transaction will be subject to the condition that NNS will have made the Offer, will have declared the Offer unconditional and will have completed settlement thereof. The reasons for the decision of the Court-appointed Directors are further explained in paragraph 5 below. Any reference to the Board in the remainder of this announcement, does not include the Court-appointed Directors, unless explicitly indicated otherwise.

1 THE OFFER

After NNS submitted a first proposal for a cash offer on 11 May 2026, the Board (excluding Nassef Sawiris and Nadia Sawiris) and NNS have been in discussions regarding a potential cash offer in connection with the Orascom Combination. The Board has carefully assessed and evaluated NNS' proposals for a voluntary all-cash offer, supported by its independent financial and legal advisers, and have considered it against alternative scenarios including a solvent wind-down.

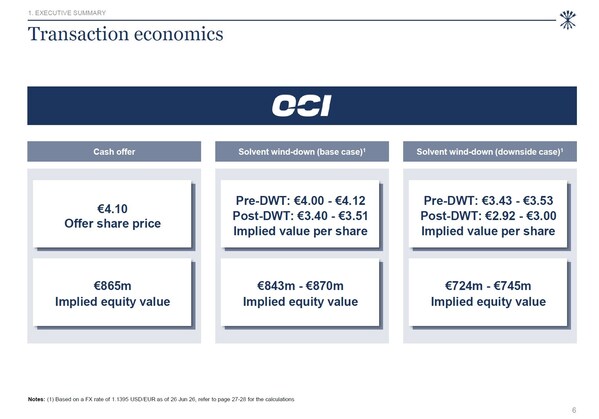

On 24 June 2026, NNS announced its intention to launch a voluntary all-cash public offer for all issued and outstanding Shares at an offer price of EUR 4.10 cum dividend per share. On 29 June 2026, NNS announced that it has submitted a draft offer memorandum to the AFM in connection with its intention to launch a voluntary all-cash public offer for all Shares at an offer price of EUR 4.10 (cum dividend) per Share. NNS also announced that it has sufficient funds readily available to finance the Offer, and the payment of fees and expenses related to the Offer, through available cash resources.

NNS furthermore announced that the obligation of NNS to declare the Offer unconditional (het bod gestand doen) will be subject to a limited number of customary offer conditions, including (i) any required competition clearances having been obtained; (ii) no AFM notification under section 5:80 Wft preventing investment firms from cooperating with settlement; (iii) no governmental order or measure prohibiting completion of the Offer; and (iv) no permanent suspension or ending of trading in the Shares on Euronext Amsterdam. NNS stated that the Offer is not subject to a minimum acceptance threshold.

For further information regarding the Offer, including the offer conditions, reference is made to the announcement from NNS dated 29 June 2026, as published on the website of OCI. OCI and NNS have not entered into a merger agreement with respect to the Offer. Further announcements will be made if a merger agreement would be concluded.

OCI will hold an EGM prior to the closing of the acceptance period of the Offer and will publish its position statement at least ten business days prior to the closing of the acceptance period of the Offer in accordance with Section 18a Paragraph 1 of the Dutch Public Takeover Decree (Besluit openbare biedingen), to inform the shareholders about the Offer.

2 REASONS FOR RECOMMENDING THE OFFER

2.1 Introduction

This section sets out the Board's reasons for recommending the Offer. References to the Board in this section in the context of the Offer or the Orascom Combination should be read as references to the board of directors of OCI, excluding Nassef Sawiris and Nadia Sawiris, who have not participated in any of the discussions, deliberations, or decision-making relating to the Offer or the Orascom Combination. Any reference to the Board in the remainder of this announcement, does not include the Court-appointed Directors, unless explicitly indicated otherwise.

Further information on the status of the Orascom Combination is included in paragraph 2.6.

The Board continues to recommend the Orascom Combination. Should shareholders be offered the opportunity to elect between tendering their Shares in the Offer or participating in the Orascom Combination, the Board encourages each shareholder to make its own assessment, having due regard to its individual circumstances and investment objectives.

2.2 Comparison against alternative scenarios

In recommending the Offer, the Board has considered the alternatives available to shareholders. Since the initiation of the strategic review in 2023, the Board has identified no attractive strategic alternative to a solvent wind-down of OCI's currently remaining business, other than the Orascom Combination on its current terms.

In order to be prepared for the scenario in which the Orascom Combination cannot be consummated, and having regard to the initial findings of the Enterprise Chamber[1] that the Board had potentially not devoted sufficient time to analysing a solvent wind-down as an alternative to the Orascom Combination, the Board engaged Alvarez & Marsal ("A&M"), an advisory firm with an internationally recognised reputation in managing complex wind-down processes, to prepare an in-depth assessment of a solvent wind-down scenario. A&M has provided the Board with a comprehensive assessment of, and planning for, a potential solvent wind-down.

In selecting A&M, the Board considered A&M's best in class expertise in managing complex wind-down processes, and full independence from OCI. The Board is satisfied that the A&M advice was provided by experts with the requisite experience and qualifications to be relied upon. A&M has significant experience in managing solvent wind down processes, including the orderly realisation of assets, settlement of liabilities, stakeholder management, and the distribution of surplus value to shareholders. Further details on A&M's credentials are set out in Annex I.

2.3 Analysis of a wind-down scenario

Based on its analysis of OCI's balance sheet, anticipated asset realisations, costs of a wind-down, and the settlement of all outstanding liabilities, A&M assessed two solvent wind-down scenarios: an Accelerated Exit Case, involving the early settlement, transfer, or insurance of outstanding exposures; and a Run-off Case, involving the managed resolution of liabilities over an extended period, with distributions made on a deferred basis.

Under these scenarios, the illustrative discounted value available for distribution to shareholders ranges from €3.21 per Share in the Accelerated Exit Case to €3.73 per Share in the Run-off Case, in each case excluding the impact of 15% Dutch dividend withholding tax ("DWT"), or €2.73 to €3.17 per Share, net of DWT. A more detailed discussion of A&M's findings is set out in paragraph 3 below.

The Board has been advised by legal counsel that, given the absence of meaningful fiscally recognized share capital, distributions in a wind-down scenario would be substantially fully subject to DWT. The Board has further been advised that proceeds received by shareholders who tender their Shares in the Offer will not be subject to DWT. The Board notes that, based on the findings of A&M, the Offer is financially superior to a solvent wind-down even for shareholders who may be eligible for a full or partial exemption from DWT on dividend distributions. A&M's findings have been a factor in the Board's decision to recommend the Offer.

2.4 Rothschild & Co fairness opinion

Upon receipt of the first non-binding proposal from NNS, the Board engaged N.M. Rothschild & Sons Limited ("Rothschild & Co") as its independent financial advisor to opine on the fairness, from a financial point of view, of a potential offer. In selecting Rothschild & Co, the Board had regard to its established knowledge of OCI gained in connection with the fairness opinion issued by it regarding the Orascom Combination.[2] The Board therefore determined that Rothschild & Co was best placed to discharge this mandate, including by virtue of its ability to deliver its analysis within the timeline that the Board considered appropriate in fulfilling its responsibilities to shareholders.

Rothschild & Co has opined that the Offer is fair, from a financial point of view to shareholders. The text of the fairness opinion and a summary of the supporting materials are attached as Annex II to this press release.

2.5 Other considerations that have informed the Board's recommendation of the Offer

The Board has reviewed the terms of the Offer and notes that NNS has publicly stated that EUR 4.10 represents its "final" offer price. The Board further notes that NNS has confirmed its willingness to sell its entire shareholding in OCI to any third party willing to make an offer that delivers greater value to all shareholders.

The Board also compared the Offer price to recent OCI share price performance. The closing price on June 24 was €3.76 per Share (undisturbed share price) and the 30-day volume-weighted average price was €3.71 per Share. The Board observes that the Offer price represents a premium of 9% and 11%, respectively, to those reference prices.

2.6 Status of the Orascom Combination

On December 9, 2025, the Board recommended the Orascom Combination to shareholders. The Board continues to recommend the Orascom Combination. The Board notes that, based on the closing price of Orascom shares on the Abu Dhabi Securities Exchange (ADX) on June 30, the implied value of the Orascom Combination for OCI Shareholders is currently approximately €6.08 per Share (€5.16 per Share, net of DWT).

The Board believes that a combination of the Offer and the Orascom Combination would be in the best interest of OCI and its stakeholders.

NNS has expressed its preference for a combined outcome in which the Offer and the Orascom Combination are both consummated. In addition, NNS has expressed an intention to offer OCI to acquire, at the market price at the time of such distribution, the Orascom shares that OCI would be required to sell in order to satisfy DWT obligations arising in connection with the distribution of Orascom shares to OCI shareholders upon consummation of the Orascom Combination. This would support market liquidity for shareholders who elect to participate in the Orascom Combination and who subsequently wish to sell their Orascom shares. The Board also notes that, during the period in which the Offer has been announced and the Orascom Combination has been approved, both the Offer and the Orascom Combination may support the OCI share price, to the benefit of shareholders who wish to sell their Shares prior to the consummation of either transaction, and may also enhance the liquidity of the Share during this period.

Following an extension by OCI, the transaction agreement between OCI and Orascom for the Orascom Combination is subject to a long-stop date of 31 December 2026. The Board further notes that NNS is no longer contractually bound to support the Orascom Combination.

3 REPORT OF ALVAREZ & MARSAL

A full summary of A&M's report, which summary has been made by A&M, is attached to this press release as Annex I. Consistent with typical solvent wind-down practice, the value impacts reflected in A&M's analysis includes not only estimated costs, but also reserves and holdbacks that may exceed liabilities or provisions currently recognised under IFRS and may be required until outstanding contractual obligations, warranties, indemnities and contingent matters are settled, transferred, insured, expired, or otherwise resolved.

4 REPORT OF ROTHSCHILD & CO

On June 30, 2026, Rothschild & Co rendered its opinion to the Board to the effect that, as of June 30, 2026, the €4.10 in cash per Share to be received by the holders of Shares in the Offer was fair, from a financial point of view to such shareholders.

The following is a summary of the material valuation analyses performed in connection with the preparation of Rothschild & Co's opinion dated June 30, 2026.

Rothschild & Co, which is authorised and regulated by the Financial Conduct Authority in the United Kingdom, is acting for OCI and no one else in relation to the Offer and will not be responsible to anyone other than OCI for providing the protections afforded to its clients nor for providing advice in relation to the Offer.

The principal valuation methodology used was a net present value calculation of dividends from a solvent wind down which combines the adjusted cash position as of May 22, 2026, and future cash flows from anticipated HoldCo costs, anticipated indemnity/liability settlements, attributable operational cash flows from OCI Nitrogen (OCIN) and proceeds from the sale of OCIN to Agrofert. The cash position, HoldCo costs and indemnity/liability settlements were discounted at 5.6% and the cash flows related to OCIN at 9.1%.

The dividends in the solvent wind down analysis are based on projected annually distributable cash flows after retaining minimum cash balances required to provide for liquidity to continue operations (both for OCIN and OCI HoldCo), remaining liabilities and exposures. The current adjusted cash position was based on management data and includes all proceeds and final settlements from the sale of OCI Clean Ammonia, OCI Ammonia Holding, and the Methanex Corporation shares as well as all other adjustments to reflect May 22, 2026, balances. An independent accounting firm reviewed the schedules.

The HoldCo costs were based on management projections reviewed by the independent accounting firm; the Fertiglobe indemnity/escrow settlements were based on probability weighted ranges, in the Base Case aligned with the audited FY2025 financial statements; and the OCIN attributable operational cash flows and sale proceeds were based on management projections. In Rothschild & Co's Base Case complete liquidation in 2031 is assumed, and in the Downside Case in 2032. The Downside Case further assumes higher HoldCo costs as a result of later liquidation, higher Fertiglobe indemnity settlements and lower OCIN attributable operational cash flows and sale proceeds. This results in higher cash reserves to be retained during the wind-down in the Downside Case which further delay dividend distributions.

This analysis resulted in a Base Case value before DWT of €4.00 to €4.12 and a Downside Case value before DWT of €3.43 to €3.53.

Additional points of reference were analysts' average target prices, which ranged from €3.75 to €3.79 based on the most recently published reports from Berenberg, Citi, Degroof Petercam, HSBC, ING Bank, JP Morgan and Kepler Cheuvreux. Rothschild & Co has also considered the twelve month and three month volume weighted average prices in the stock market which ranged from €3.63 to €3.64; the 12 month high and low prices in the stock market which were €2.65 to €5.04; the 3 month high and low prices in the stock market which were €3.32 and €4.03; and, the current value of the proposed Orascom transaction which was €6.07 before DWT and €5.16 net of DWT.

The Rothschild & Co and A&M analyses are based on broadly similar distributable cash and dividend discount frameworks. The valuation differences are driven primarily by different assumptions regarding the timing and discount rate of cash available for distribution, rather than by fundamentally different standalone asset values.

In considering Rothschild & Co's analysis, shareholders should note that the valuation references used in connection with the original Orascom Combination and the current Offer are not directly comparable. Rothschild & Co's December 2025 fairness opinion was provided in the context of a share-for-share combination with Orascom Construction and assessed the fairness, from a financial point of view, of the consideration to be received by OCI under that transaction. The agreed exchange ratio reflected a relative valuation exercise for OCI and Orascom Construction and was intended to determine the relative contributions of each company to the Orascom Combination.

5 STATEMENT BY THE COURT-APPOINTED DIRECTORS

The Court-appointed Directors announce that, having completed their assessment of the transaction between OCI and Orascom in conjunction with the NNS Offer, they have decided to consent to the convocation of an extraordinary general meeting of the Company to approve the OCI-Orascom transaction. The resolution to approve the OCI-Orascom transaction will be subject to the condition that NNS will have made the Offer, will have declared the Offer unconditional and will have completed settlement thereof.

The Court-appointed Directors note that certain minority shareholders have indicated a preference for participating in the OCI-Orascom transaction, while others have expressed a preference for a cash exit. In reaching their decision, the Court-appointed Directors have taken both perspectives into account.

5.1 Mandate of the Court-appointed Directors

The Court-appointed Directors have been appointed by the Enterprise Chamber of the Amsterdam Court of Appeal ("Enterprise Chamber") on 22 January 2026 as independent non-executive directors of OCI with a special mandate. That mandate requires them to independently assess the preparation of the transaction with Orascom Construction, or any other transaction with Orascom Construction requiring shareholder approval, and to ensure that the Board fulfils its obligations towards OCI and all its stakeholders, including, and in particular, its minority shareholders.

In carrying out their mandate, the Court-appointed Directors operate fully independently from the Company's controlling shareholder. This independence has been, and remains, pivotal to their role.

Since their appointment, the Court-appointed Directors have engaged extensively with a broad range of stakeholders. They have reviewed a considerable amount of documentation and have asked detailed questions about the background, preparation and terms of the OCI-Orascom transaction and the broader strategic context. The Court-appointed Directors have also appointed their own independent legal advisor, as well as AXECO Corporate Finance ("AXECO") as their own independent financial advisor.

Based on the analysis of all available information, the Court-appointed Directors have formed a considered view in respect of the OCI-Orascom transaction.

5.2 OCI-Orascom transaction

The Court-appointed Directors are of the view that, in the period up to the Enterprise Chamber's decision, the interests of OCI's minority shareholders were not sufficiently reflected in the process, structure and the Board's decision-making in respect of the OCI-Orascom transaction.

In reaching this view, the Court-appointed Directors have considered that (i) the transaction structure was atypical for Dutch listed companies, (ii) the controlling shareholder was effectively in a position to approve the OCI-Orascom transaction at OCI's extraordinary general meeting, without the support of any other OCI shareholder, (iii) the structure required all OCI shareholders to exchange their investment in a Dutch listed company for an investment in a company listed on a stock exchange outside the EEA, without an upfront cash exit alternative being offered, (iv) not all OCI shareholders would be able to receive their Orascom Construction shares through their existing securities accounts, (v) the transaction structure was such that the controlling shareholder would ultimately not incur Dutch dividend withholding tax, whereas a significant proportion of other OCI shareholders would, and (vi) OCI requested its financial advisor to issue a fairness opinion in respect of the OCI-Orascom exchange ratio, without the additional request to also consider the value ultimately received by OCI's shareholders.

5.3 NNS Offer

On 24 June 2026, NNS announced its intention to launch an all-cash offer, at an offer price of EUR 4.10 (cum dividend) per Share.

On 25 June 2026, the Court-appointed Directors announced that they welcomed the Offer, as it represented a potentially meaningful step towards resolving the impasse surrounding the OCI-Orascom transaction, and that they were continuing to consider the proposal. In that context, the Court-appointed Directors announced that the adequacy of the Offer would be a relevant consideration in their ongoing assessment of the OCI-Orascom transaction.

On 26 June 2026, NNS announced its confirmation that the offer price of EUR 4.10 (cum dividend) per Share represents its final offer. On 29 June 2026, NNS announced that it had submitted a draft offer memorandum to the AFM in connection with the Offer, with limited conditionality.

At the request of the Court-appointed Directors, AXECO conducted a value assessment of a solvent winddown scenario. In that respect, AXECO has assessed the known assets and liabilities of the Company in a liquidation scenario. Particular attention was given to the Fertiglobe indemnities. The Court-appointed Directors, together with their independent legal advisor and AXECO, examined in detail the probability of a release of the Fertiglobe-related escrow to OCI, and discussed their views with the Company and the Company's advisors. On that basis and given the significant uncertainty surrounding the outcome of the underlying Fertiglobe indemnity matters, the Court-appointed Directors have concluded that at this point in time no value can be attributed to a release of the escrow amount for the purposes of this assessment.

AXECO has issued a fairness opinion in respect of the Offer. AXECO has concluded that the offer price of EUR 4.10 (cum dividend) per Share is fair, from a financial point of view, to the OCI shareholders (other than NNS and any of its affiliates). The AXECO fairness opinion is attached as Annex III to this press release.

Based on the independent valuation analyses performed by AXECO, the Court-appointed Directors have reached the conclusion that the offer price is not unreasonable from a financial point of view. However, they conclude that the offer price is not sufficiently convincing for them to recommend to the OCI shareholders to tender their Shares pursuant to the Offer. Nevertheless, as the Offer in itself provides cash optionality for OCI shareholders, the Court-appointed Directors do support the Offer, be it with a neutral opinion in respect of the offer price.

5.4 Conclusion

The Court-appointed Directors are of the view that the Offer is a relevant and meaningful addition to the OCI-Orascom transaction. They consider that the combination of the OCI-Orascom transaction and the Offer gives adequate and reasonable weight to the interests of OCI's minority shareholders.

In reaching this conclusion, the Court-appointed Directors have also taken into account the appreciation in the share price of Orascom Construction, which has provided more clarity as to the value proposition embedded in the OCI-Orascom share exchange ratio. A number of OCI's minority shareholders have recently indicated that, for that reason, they are in favour of the OCI-Orascom transaction.

The Court-appointed Directors have further considered that the only tangible alternative to the OCI-Orascom transaction is a solvent wind-down of OCI. Such a scenario would involve a lengthy process expected to extend until at least 2031, would entail significant costs and material uncertainty as to the ultimate liquidation proceeds available for distribution to shareholders, and would likely result in Dutch dividend withholding tax being levied on distributions to a significant proportion of OCI's minority shareholders, reducing the net amount received by those shareholders by 15% (at current rates). A solvent wind-down scenario would therefore not appear to represent a financially superior outcome for shareholders when compared to the OCI-Orascom transaction in combination with the Offer.

On that basis, the Court-appointed Directors have decided to consent to the convocation of an extraordinary general meeting of the Company, to be convened simultaneously with the publication of the offer memorandum in respect of the Offer by NNS, to approve the OCI-Orascom transaction. The resolution to be presented to shareholders will be subject to the condition that NNS will have made the Offer and will have declared the Offer unconditional (gestanddoen) and that settlement of the Offer will have taken place.

Advisers

Alvarez & Marsal has provided OCI's Board with an in-depth assessment of a solvent wind-down scenario, while N.M. Rothschild & Sons Limited served as its independent financial advisor to opine on the fairness, from a financial point of view, of a potential offer. De Brauw Blackstone Westbroek N.V. acted as legal advisor to OCI, Wakkie & Perrick B.V. also provided legal advice to OCI's board. AXECO Corporate Finance B.V. and Freshfields LLP provided financial and legal advice, respectively, to the Court-appointed independent non-executive directors.

Important information

This press release contains information within the meaning of Article 7(1) of the EU Market Abuse Regulation.

ABOUT OCI GLOBAL

Learn more about OCI at www.oci-global.com. You can also follow OCI on LinkedIn.

[1] The decision of the Enterprise Chamber (Amsterdam Court of Appeal) is available on our website in the designated section regarding the Orascom Combination.

[2] Rothschild & Co's fairness opinion on the proposed acquisition by Orascom of all of the issued share capital of a to be formed subsidiary of OCI, holding substantially all of the business, assets and liabilities of OCI, as set out in a sale and purchase agreement to be entered into by Orascom and OCI, is available on OCI's website in the designated section regarding the Orascom Combination.

OCI N.V. recommends the unsolicited all-cash Offer from NNS at EUR 4.10 per share. The Court-appointed Directors consent to the convocation of an extraordinary general meeting to submit the OCI-Orascom transaction to a shareholder vote.

Source: OCI Global Related Stocks: EuronextAmsterdam:OCI